Official Loan Agreement Form for California

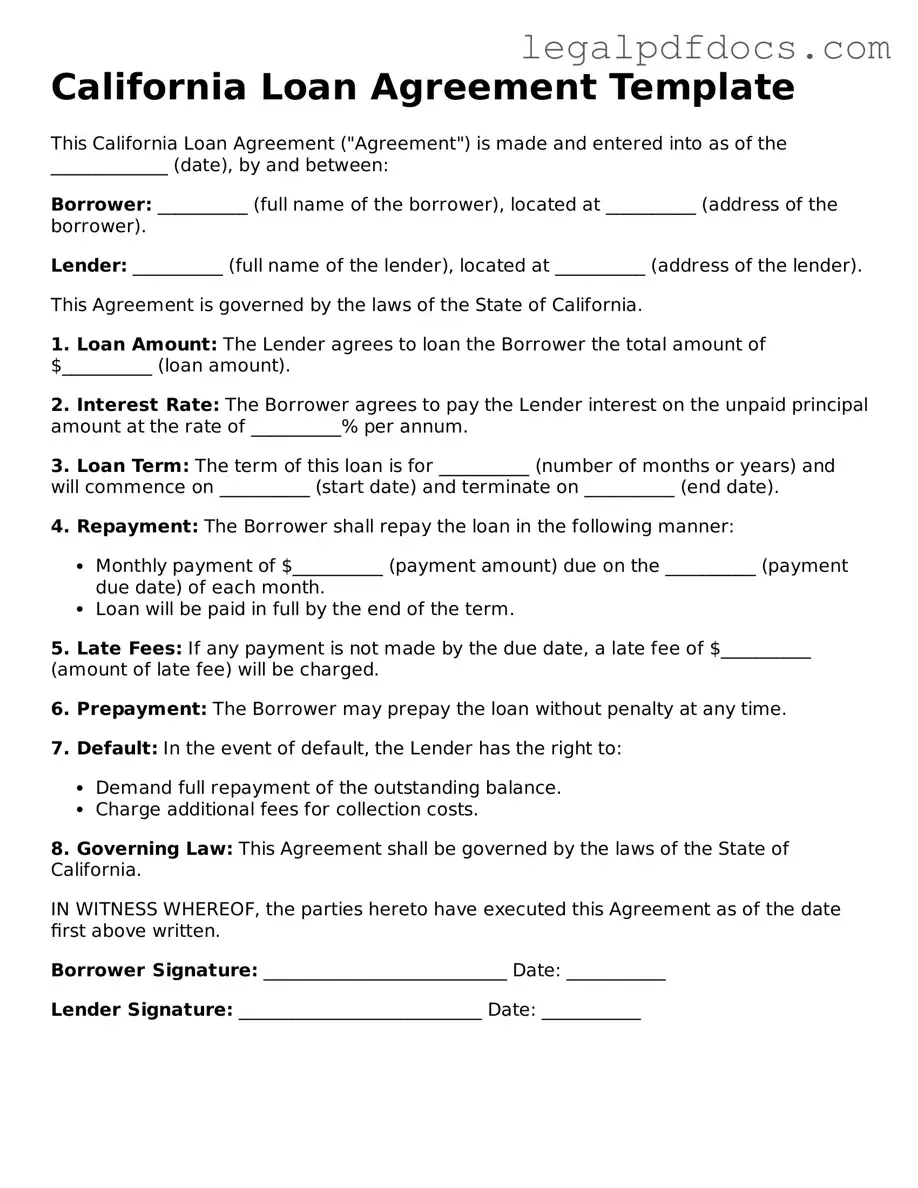

The California Loan Agreement form serves as a crucial document for individuals and entities engaging in lending transactions within the state. This form outlines the terms and conditions under which a borrower receives funds from a lender, ensuring that both parties have a clear understanding of their rights and obligations. Key components of the agreement include the loan amount, interest rate, repayment schedule, and any collateral that may secure the loan. Additionally, the form addresses potential fees, default conditions, and remedies available to the lender in case of non-compliance. By clearly delineating these elements, the California Loan Agreement helps to minimize misunderstandings and disputes, fostering a more transparent borrowing process. Whether for personal loans, business financing, or real estate transactions, this form plays an essential role in facilitating secure and responsible lending practices throughout California.

Dos and Don'ts

When filling out the California Loan Agreement form, attention to detail is crucial. Here are five important dos and don’ts to keep in mind:

- Do read the entire agreement carefully before signing.

- Do provide accurate and complete information to avoid delays.

- Do ask questions if any part of the agreement is unclear.

- Don't rush through the form; take your time to ensure everything is correct.

- Don't leave any sections blank unless instructed to do so.

By following these guidelines, you can help ensure a smoother process in securing your loan.

How to Use California Loan Agreement

Completing the California Loan Agreement form requires careful attention to detail. Each section must be filled out accurately to ensure that the agreement is valid and enforceable. Below are the steps to guide you through the process of filling out this form.

- Begin by entering the date at the top of the form.

- Provide the full name and address of the borrower in the designated section.

- Next, fill in the lender's full name and address.

- Specify the principal amount of the loan in the appropriate field.

- Indicate the interest rate applicable to the loan.

- Detail the loan term, including start and end dates.

- Include any repayment terms, such as monthly payment amounts and due dates.

- State the purpose of the loan clearly.

- Sign and date the form at the bottom, ensuring all parties involved do the same.

After completing these steps, review the form for accuracy before submitting it to the relevant parties. This will help prevent any misunderstandings or disputes in the future.

Find Popular Loan Agreement Forms for US States

Loan Agreement Template Texas - Borrowers should ensure they understand their obligations before signing the form.

Promissory Note Illinois - Terms for renewal or extension of the loan can be included.

Promissory Note Georgia - Describes the rights of the borrower to access loan information.

Documents used along the form

When entering into a loan agreement in California, several additional forms and documents may be necessary to ensure clarity and legal compliance. These documents help outline the terms of the loan, protect the interests of both parties, and provide a clear framework for the transaction. Below are some commonly used documents that accompany a California Loan Agreement.

- Promissory Note: This is a written promise from the borrower to repay the loan under specified terms. It includes details such as the loan amount, interest rate, and repayment schedule.

- Security Agreement: If the loan is secured by collateral, this document outlines the specific assets that back the loan. It provides the lender with rights to the collateral if the borrower defaults.

- Disclosure Statement: This document provides important information about the loan, including the total cost, interest rates, and any fees involved. It ensures that the borrower understands the financial implications of the loan.

- Loan Application: This form collects personal and financial information from the borrower. It helps the lender assess the borrower's creditworthiness and ability to repay the loan.

- Guaranty Agreement: In some cases, a third party may agree to guarantee the loan. This document outlines the guarantor's commitment to repay the loan if the borrower defaults.

Each of these documents plays a vital role in the loan process, ensuring that all parties are informed and protected. It is advisable to carefully review each document and seek assistance if needed to ensure a smooth transaction.

Misconceptions

Many individuals have misunderstandings about the California Loan Agreement form. Here are seven common misconceptions:

-

All loan agreements are the same.

Each loan agreement can differ significantly based on terms, interest rates, and conditions. It's crucial to review each document carefully.

-

Verbal agreements are sufficient.

A written loan agreement is essential for legal protection. Verbal agreements can lead to disputes that are hard to prove.

-

Only lenders need to understand the form.

Both borrowers and lenders should fully comprehend the terms. Ignorance of the details can lead to financial issues down the line.

-

Signing the agreement means all terms are negotiable.

While some terms may be negotiable, others are often set in stone. Always clarify what can be adjusted before signing.

-

Loan agreements are only for large sums of money.

Even small loans require a formal agreement. Protecting both parties is vital, regardless of the amount involved.

-

Once signed, the agreement cannot be changed.

Modifications can be made if both parties agree. Document any changes in writing to ensure clarity and legal standing.

-

The California Loan Agreement form is only for personal loans.

This form can also apply to business loans and other types of financing. Its versatility makes it useful across various lending scenarios.

PDF Specifications

| Fact Name | Description |

|---|---|

| Purpose | The California Loan Agreement form is used to outline the terms and conditions of a loan between a lender and a borrower. |

| Governing Law | This agreement is governed by California state laws, specifically the California Civil Code. |

| Loan Details | It includes important details such as the loan amount, interest rate, repayment schedule, and any collateral involved. |

| Signatures Required | Both parties must sign the agreement to indicate their acceptance of the terms outlined in the document. |

| Default Terms | The agreement typically outlines what constitutes a default and the remedies available to the lender in such cases. |

Key takeaways

When filling out and using the California Loan Agreement form, there are several important points to keep in mind. These takeaways can help ensure that the agreement is clear, enforceable, and protects the interests of both parties involved.

- Identify the Parties: Clearly state the names and addresses of both the lender and the borrower at the beginning of the agreement.

- Loan Amount: Specify the exact amount of money being loaned. This should be clearly stated in both numbers and words.

- Interest Rate: Include the interest rate being charged on the loan. Make sure it complies with California's usury laws.

- Payment Terms: Outline the payment schedule, including due dates and the method of payment. This should be straightforward to avoid confusion.

- Default Conditions: Define what constitutes a default on the loan. This section should explain the consequences if the borrower fails to make payments.

- Governing Law: Indicate that the agreement will be governed by California law. This is important for legal clarity.

- Signatures: Ensure both parties sign the agreement. This makes the contract legally binding.

- Witness or Notary: Consider having the agreement witnessed or notarized. This can add an extra layer of legitimacy.

- Keep Copies: Both parties should retain copies of the signed agreement for their records. This can help resolve any disputes that may arise later.