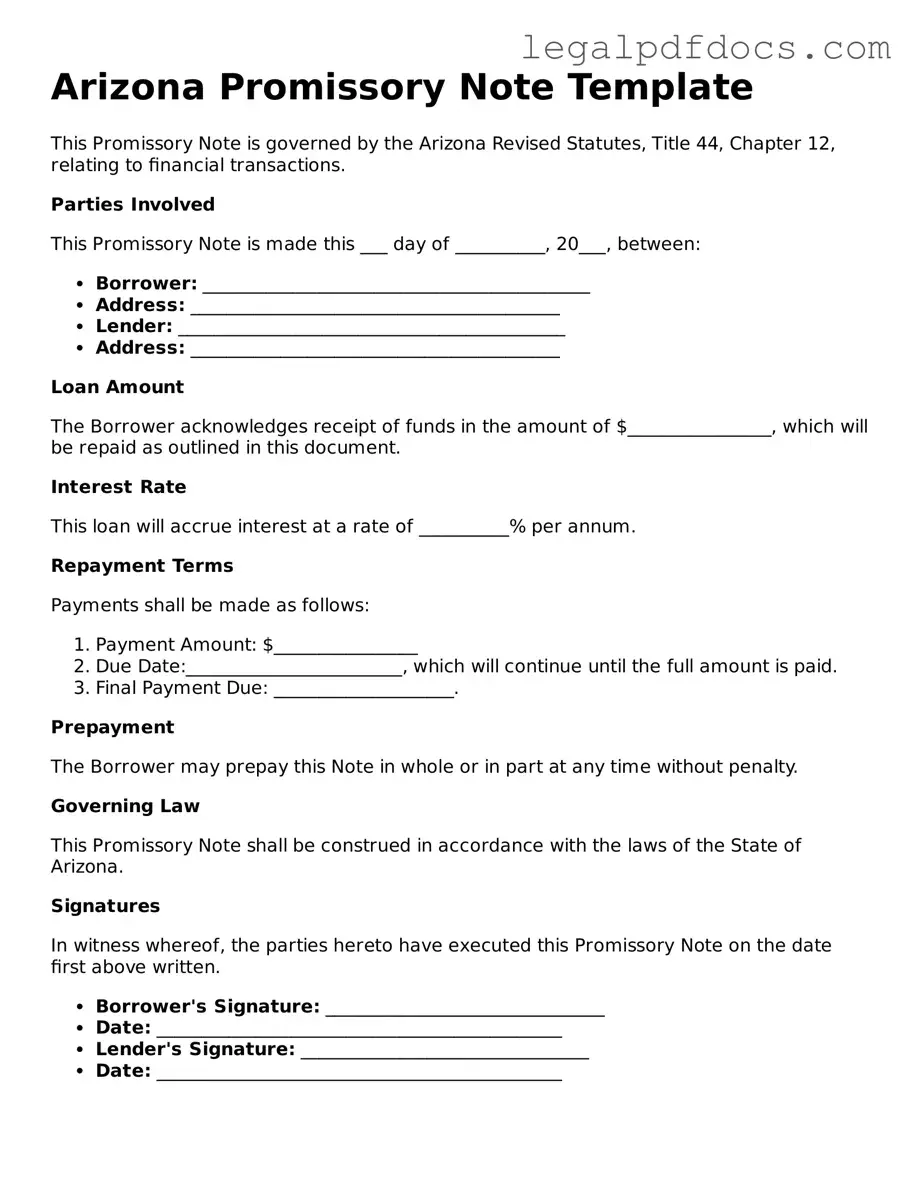

Official Promissory Note Form for Arizona

The Arizona Promissory Note form serves as a crucial financial document that outlines the terms of a loan between a borrower and a lender. This form typically includes key details such as the principal amount borrowed, the interest rate, repayment schedule, and any applicable fees. It also specifies the consequences of default, ensuring that both parties understand their rights and obligations. Additionally, the form may require signatures from both the borrower and lender, solidifying the agreement and providing legal protection. By utilizing this standardized document, individuals and businesses can facilitate smoother transactions and minimize potential disputes, making it an essential tool in the realm of personal and commercial finance in Arizona.

Dos and Don'ts

When filling out the Arizona Promissory Note form, it is important to approach the task with care and attention to detail. Here are some guidelines to help you navigate the process effectively:

- Do ensure that all parties involved are clearly identified. Include full names and addresses to avoid any confusion.

- Do specify the loan amount and the terms of repayment. Clarity in these details can prevent misunderstandings later on.

- Don't leave any sections blank. Each part of the form should be completed to ensure it is legally binding and enforceable.

- Don't use vague language. Be precise in your wording to ensure that all parties understand their obligations and rights.

By adhering to these guidelines, you can help ensure that your Promissory Note is both effective and legally sound.

How to Use Arizona Promissory Note

After gathering all necessary information, you are ready to fill out the Arizona Promissory Note form. This document will require specific details about the loan agreement between the borrower and the lender. Follow these steps to ensure you complete the form accurately.

- Title the Document: At the top of the form, write "Promissory Note" to clearly indicate the purpose of the document.

- Enter the Date: Write the date on which the note is being executed. This is important for record-keeping.

- Identify the Borrower: Fill in the full name and address of the borrower. This identifies who is responsible for repaying the loan.

- Identify the Lender: Provide the full name and address of the lender. This is the person or entity providing the loan.

- Loan Amount: Clearly state the total amount of money being borrowed. Make sure this is accurate and reflects the agreed-upon sum.

- Interest Rate: Specify the interest rate applicable to the loan. Indicate whether it is fixed or variable.

- Payment Terms: Outline the payment schedule, including the frequency of payments (monthly, quarterly, etc.) and the total number of payments to be made.

- Due Date: Indicate the final due date for the loan repayment. This is when the borrower must repay the entire amount.

- Signatures: Both the borrower and lender must sign and date the document. This signifies agreement to the terms outlined in the note.

Once completed, review the form for accuracy. Ensure all information is correct before making copies for both parties. Keep the original in a safe place.

Find Popular Promissory Note Forms for US States

Kansas Promissory Note - The enforceability of a promissory note may vary based on jurisdictional laws.

Texas Promissory Note Template - Having clear payment terms in the Promissory Note reduces misunderstandings between the lender and borrower.

Promissory Note California - Understanding the terms before signing a promissory note is crucial for both parties.

Promissory Note Template Georgia - Knowing how to properly fill out a Promissory Note helps avoid future complications.

Documents used along the form

When entering into a financial agreement involving a promissory note in Arizona, several other forms and documents often accompany it. Each of these documents serves a specific purpose, ensuring clarity and legal compliance in the transaction. Below is a list of commonly used forms that complement the Arizona Promissory Note.

- Loan Agreement: This document outlines the terms of the loan, including the amount borrowed, interest rates, and repayment schedule. It provides a comprehensive understanding of the obligations of both the lender and the borrower.

- Security Agreement: If the loan is secured by collateral, this agreement details the assets pledged as security. It specifies what happens if the borrower defaults on the loan, protecting the lender's interests.

- Personal Guarantee: In cases where a business borrows money, a personal guarantee may be required from an individual. This document makes the individual personally liable for the debt if the business fails to repay.

- Disclosure Statement: This statement provides important information about the loan, such as fees, terms, and conditions. It helps ensure that the borrower understands the financial implications of the agreement.

- Amortization Schedule: This schedule breaks down each payment into principal and interest components over the life of the loan. It aids borrowers in understanding how their payments will affect the balance over time.

- Default Notice: This document is used to inform the borrower that they have defaulted on their loan obligations. It outlines the consequences of default and any actions the lender may take.

- Release of Liability: If a loan is paid off or otherwise settled, this document formally releases the borrower from any further obligations under the promissory note, providing peace of mind.

- Assignment of Note: This form allows the lender to transfer their rights under the promissory note to another party. It ensures that the new holder of the note has all necessary rights to collect payments.

Understanding these accompanying documents is crucial for both lenders and borrowers. They help create a clear framework for the transaction, ensuring that all parties are aware of their rights and responsibilities. By using these forms in conjunction with the Arizona Promissory Note, individuals can navigate their financial agreements with greater confidence and security.

Misconceptions

Understanding the Arizona Promissory Note form can be challenging due to various misconceptions. Here are five common misunderstandings:

-

All Promissory Notes are the Same:

Many believe that all promissory notes are identical. In reality, the terms and conditions can vary significantly based on the agreement between the parties involved.

-

A Promissory Note Must Be Notarized:

Some individuals think that notarization is a requirement for a promissory note to be valid. While notarization can provide additional legal protection, it is not mandatory in Arizona.

-

Only Lenders Can Create Promissory Notes:

There is a misconception that only financial institutions or lenders can draft promissory notes. In fact, any individual or entity can create a promissory note as long as it meets the necessary legal requirements.

-

Promissory Notes Are Non-Enforceable:

Some people believe that promissory notes lack enforceability. However, when properly executed, they are legally binding documents that can be enforced in a court of law.

-

Interest Rates Are Fixed:

There is a common assumption that interest rates on promissory notes must remain fixed. However, parties can negotiate terms that allow for variable interest rates, depending on their agreement.

PDF Specifications

| Fact Name | Description |

|---|---|

| Definition | An Arizona Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time. |

| Governing Law | The Arizona Promissory Note is governed by Arizona Revised Statutes, Title 47, which covers commercial transactions. |

| Parties Involved | The note involves at least two parties: the borrower (maker) and the lender (payee). |

| Interest Rate | The interest rate can be fixed or variable, and it should be clearly stated in the note. |

| Repayment Terms | Repayment terms must be specified, including the payment schedule, due dates, and any late fees. |

| Signatures | The note must be signed by the borrower to be enforceable, and it is advisable for the lender to sign as well. |

Key takeaways

When dealing with a Promissory Note in Arizona, understanding the key elements can make the process smoother. Here are some important takeaways to keep in mind:

- Understand the Purpose: A Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It serves as a written record of the debt.

- Include Essential Information: The note should clearly state the names of both the borrower and the lender, the amount borrowed, and the interest rate, if applicable.

- Specify Payment Terms: Clearly outline when payments are due, the frequency of payments, and the total duration of the loan. This helps avoid misunderstandings later on.

- Consider Collateral: If the loan is secured, describe the collateral being offered. This provides additional security for the lender.

- Be Aware of State Laws: Arizona has specific laws governing promissory notes. Familiarize yourself with these to ensure compliance and enforceability.

- Signatures Matter: Both parties should sign the note. A signature indicates agreement to the terms and can be crucial in case of disputes.

- Keep Copies: After completing the note, both the borrower and lender should keep copies. This ensures that both parties have access to the agreed-upon terms.

- Consult a Professional: If there are uncertainties about the terms or legal implications, consider seeking advice from a legal professional to ensure everything is in order.

By keeping these key points in mind, you can navigate the process of filling out and using the Arizona Promissory Note form with greater confidence.